unified estate and gift tax credit 2020

The federal estate tax gift and estate tax exemption amount is now 114 million indexed for inflation which is an all-time high. For any gifts that exceed 15000 per individual you will need to file a Gift Tax return even though no taxes will be due unless you exceed the unified estate and gift tax exemption 1158 million in 2020.

How The Unified Tax Credit Maximizes Wealth Transfer Blog Jenkins Fenstermaker Pllc

For 2020 the basic exclusion amount will go up 180000 from 2019 levels to a new total of 1158 million.

. If a gift is given as a present interest gift meaning it is given outright to a person then the amount is not added into your total lifetime unified gift and estate tax credit. How does the unified estate tax credit work. In other words the unified credit is one pool of credit.

48600 up until first of month of birthday. A person giving the gifts has a lifetime exemption from paying taxes on those gifts until they reach a certain figure. You can give up to this amount in money or property to any individual per year without incurring a gift tax.

The annual gift tax exclusion is 16000 for tax year 2022 up from 15000 from 2018 through 2021. The unified tax credit is designed to decrease the tax bill of the individual or estate. Then there is the exemption for gifts and estate taxes.

The unified credit is per person but a married couple can combine their exemptions. In addition to the unified tax credit individuals can give up to 15000 a year to a recipient or recipients 15000 per gift to as many recipients regardless of how many people you gift and not have to pay a gift tax. The previous limit for 2020 was 1158 million.

The IRS announced new estate and gift tax limits for 2021 during the fall of 2020. It can be used by taxpayers before or after death integrates both the gift and estate taxes into one tax system is adjusted for inflation and has no income limit. The 1206 million exemption applies to gifts and estate taxes combinedany portion of the exemption you use for gifting will reduce the amount you can use for the estate tax.

The unified tax credit is designed to decrease the tax bill of the individual or estate. For 2021 that lifetime exemption amount is 117 million. The applicable credit amount is commonly referred to as the Unified Credit because it is both unified ie it is a single amount that is applied to transfers otherwise subject to either the gift tax or the estate tax and a tax credit ie it reduces the amount of tax owed.

The lifetime gift tax exclusion in 2020 is 1158 million meaning the federal tax law applies the estate tax to any. 2020 1 for every additional 3 earned. The tax is then reduced by the available unified credit.

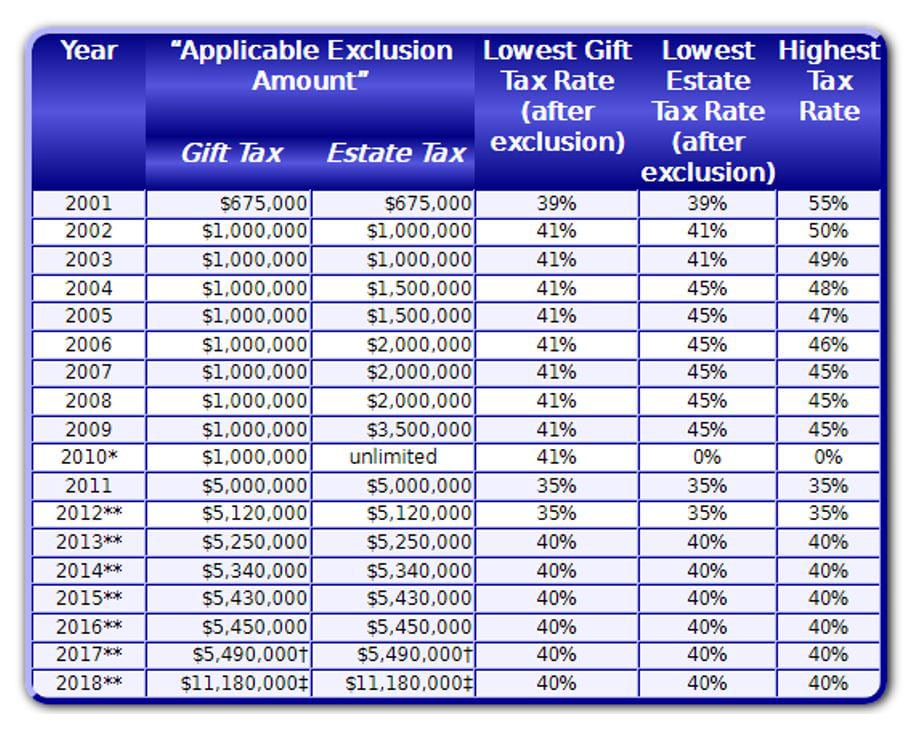

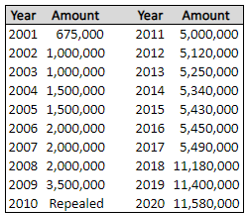

For 2009 tax returns every American received an automatic unified tax credit against federal estate and gift taxes of 1455800 which is equivalent to transferring 35 million tax-free to your heirs. Your gifts can total 30000 for the year if you want to give two people each the annual exclusion amount. Since 2000 the estate and gift tax collectively called the transfer tax has gone from an exemption of 675000 and a top marginal rate of 55 to a n.

A married couple can transfer twice that amount to children or others or 228 million without any federal gift and estate tax. Not over 2600 10 of taxable income. Gift and Estate Tax Exemptions The Unified Credit.

The estate and gift tax exemption is. Learn more about estate taxes by. This is called the unified credit.

As of 2021 married couples can exempt 234 million In 2022 couples can exempt 2412 million. In other words the unified credit is one pool of credit. In 2020 after adjustment for inflation it was raised to 1158 million for individuals and 2316 million for a married couple.

Any tax due is determined after applying a credit based on an applicable exclusion amount. Highest estate and gift tax rate. The gift tax will likely only be used to document.

11580000 Generation-skipping transfer tax exclusion. A key component of this exclusion is the basic exclusion amount BEA. That number is used to calculate the size of the credit against estate tax.

For 2022 the exemption increases to 1206 for individuals and 2412 for married couples filing jointly up from 117 million and 234 million respectively for 2021. In other words use it or lose it. It can be used by taxpayers before or after death integrates both the gift and estate taxes into one tax system is adjusted for inflation and has no income limit.

If you made a 1 million gift to a child during your lifetime that would be subtracted from what you could transfer to anyone at death ie under current law that would leave you with 4340000 to transfer to anyone estate and gift tax free. Unused credit can pass to the surviving spouse if decedent spouse elects on Form 706. The federal exemption amount is also now portable between spouses.

Citizen received the same exemption credit so that you could as a couple give a full 7 million to your heirs free of the. The IRS refers to this as a unified credit Each donor the person making the gift has a separate lifetime exemption that can be used before any out-of-pocket gift tax is due. Most relatively simple estates cash publicly traded securities small amounts of other easily valued assets and no special deductions or elections or jointly held property do not require the filing of an estate tax return.

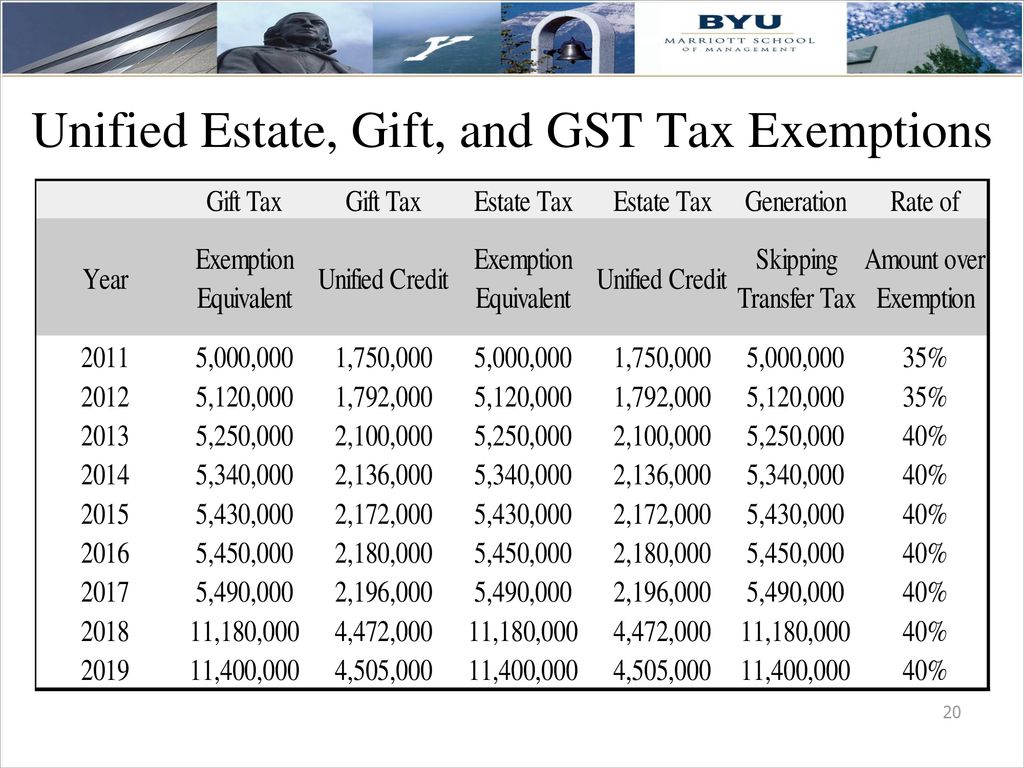

Gift Tax Credit Equivalent 2141800 4417800 4505800 4577800. For 2021 the estate and gift tax exemption stands at 117 million per person. The Internal Revenue Service announced today the official estate and gift tax limits for 2020.

If you made a 1 million gift to a child during your lifetime that would be subtracted from what you could transfer to anyone at death ie under current law that would leave you with 4340000 to transfer to anyone estate and gift tax free. If you were married your spouse also a US. The amount of the Unified Credit is currently higher than it has ever been while an estate tax is.

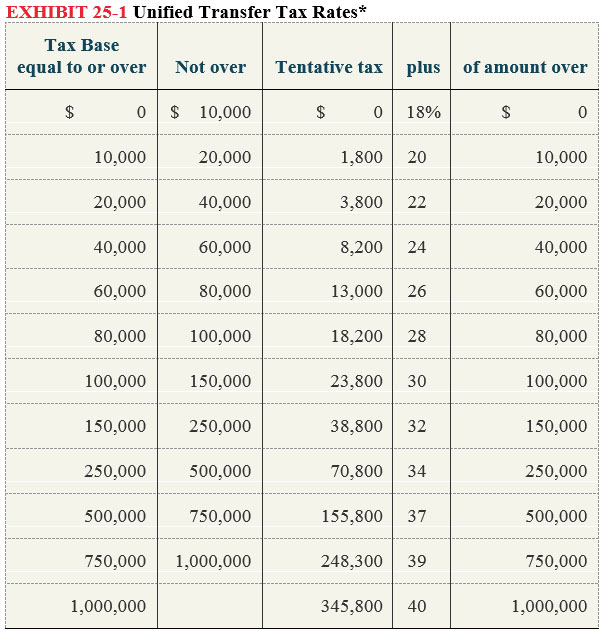

The IRS places restrictions on gifts given to people other than your spouse. The lifetime gift tax exclusion was expanded under the Tax Cuts and Jobs Act and with an inflation adjustment in 2020. In general the Gift Tax and Estate Tax provisions apply a unified rate schedule to a persons cumulative taxable gifts and taxable estate to arrive at a net tentative tax.

Gifts and estate transfers that exceed 1206 million are subject to tax. Instead these gifts are limited to 15000 per person annually. Unified estate and gift tax credit amount.

![]()

Irs Alert Update New 2020 Federal Estate Gift Tax Limits Announced By The Irs David M Frees Iii

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Gift Tax Unified Tax Credit Estate Tax Corporate Income Tax Course Cpa Exam Far Youtube

What It Means To Make A Gift Under The Federal Gift Tax System Agency One

Historical Estate Tax Exemption Amounts And Tax Rates 2022

Gift Tax Exemption Lifetime Gift Tax Exemption The American College Of Trust And Estate Counsel

Estate And Gift Tax Calculation Examples Video Youtube

Estate Tax Primer For German Investors In U S Real Estate Partnerships Dallas Business Income Tax Services

Tax Related Estate Planning Lee Kiefer Park

/ScreenShot2020-02-03at1.41.37PM-322605a2b23a49598d9cdf9faee0a97a.png)

Form 706 United States Estate And Generation Skipping Transfer Tax Return Definition

Solved Gabriel Had A Taxable Estate Of 8 4 Million When He Chegg Com

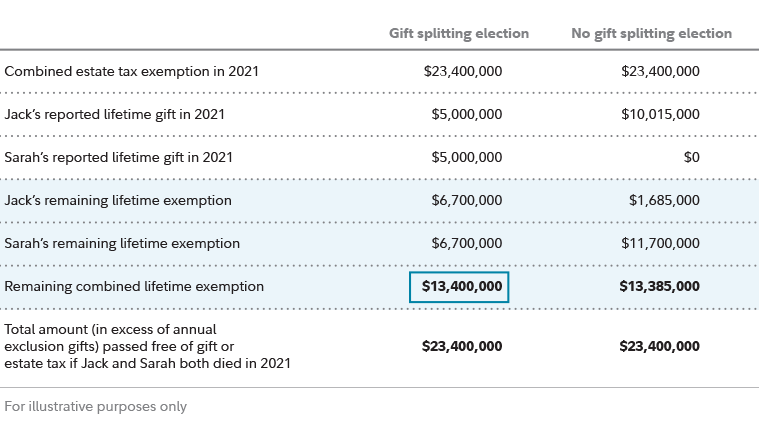

Estate Planning Strategies For Gift Splitting Fidelity

2021 Cost Of Living Adjustments And Estate Gift Tax Limits Cpa Boston Woburn Dgc

A Look At 2020 Cost Of Living Adjustments And Estate Gift Tax Limits Cpa Boston Woburn Dgc

History Of The Unified Tax Credit Apple Growth Partners

/How-Is-the-Gift-Tax-Calculated-3505674-v2-HL-cf2d3bd9ac04413ba108e6b0a44f0f39.png)

Gift Tax How Much Is It And Who Pays It

Estate Tax Primer For German Investors In U S Real Estate Partnerships Dallas Business Income Tax Services

What Is Estate Tax Quora

Personal Finance Another Perspective Ppt Download